Image

Properly capitalized farms and food businesses are critical for a healthy food system. Food system businesses need different kinds of capital depending on their stage of growth, scale of operation, and the markets into which they sell. In part due to the aging of our population, Vermont is experiencing an unprecedented generational transfer of farmland and food businesses. We need to develop new business models, and support access to affordable farmland for new and beginning farmers and young entrepreneurs to take over food businesses, all of which require significant capital and business acumen for success. Critical to this process is connecting the next generation of values-driven investors with opportunities to support farms, food producers, and food system businesses, through a variety of capital provider organizations and through programs that educate new investors.

Strengthening the state and regional food system is one of the most important paths for broad and sustainable wealth creation in rural communities, yet Vermont farm and food businesses are forced to rely on a more limited financing landscape than businesses in other sectors.

There is a deep interrelationship between matching the right kind of capital with the right capital structure and provider, as well as individuals and/or networks that can provide that capital.

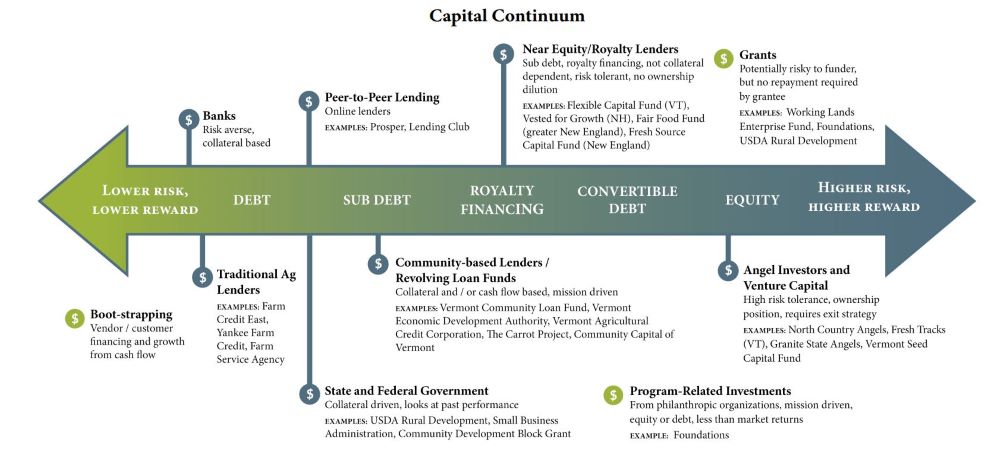

Capital can take many forms, as shown in the capital continuum diagram. Financial capital can be structured as debt, equity, grants, and more. The maturity of different types of businesses within the food system can impact access to capital, as well as dictate the form of capital that is most suitable. For instance, for food manufacturing businesses that are growing or pivoting their business and expanding facilities and/or distribution, there is often a lag time between when investments are made in a new facility or equipment and when revenues are generated from that investment. This leads to cash flow challenges as the business grows and requires additional working capital that is patient and flexible.

From 2008 - 2018, a suite of new and diverse forms of capital have become available to Vermont farm and food businesses. Alongside the growth in Yankee Farm Credit and Vermont Agricultural Credit Corp (VACC) portfolio of loans over the last decade, new lending programs, such as the Vermont Community Loan Fund’s (VCLF) Food, Farms & Forest Fund, have been developed. The advent of crowdfunding, complemented by the changes to the Vermont Small Business Offering Exemption, have allowed food system businesses the ability to seek capital directly from individual investors. One example is Milk Money Vermont, a platform for businesses to raise capital from Vermont investors in amounts and at a scale that are accessible to the full range of individual investors.

The Vermont Working Lands Enterprise Fund is another example of an important new source of capital, providing grant funding to strengthen and grow the businesses connected to Vermont’s working landscape. Since its inception in 2012, the Fund has distributed over $5.3 million to 184 agriculture and forestry projects.

For a full Farm and Food Enterprise Financing Inventory of Capital Providers, see vtfarmtoplate.com/resources/food-system-financing-inventory.

Demographics and market shifts are accelerating the pace of generational farm transitions. There are multiple costs when farms transition, including the farm land transfer, the transaction, and the start-up costs of the new farm. New and beginning farmers are attempting to access farmland on which to develop their businesses, but as the historic mechanisms of family inheritance and transferable dairy markets have become the rare exception, innovative lease-to-own models are emerging that enable incoming farmers to build equity and working capital while they grow markets and customers.

There are myriad lending programs supporting Vermont value-added food businesses. Companies with hard assets (e.g., equipment, real estate) are commonly able to finance early growth in small amounts through these sources of debt. As food system businesses scale and grow, they can be at risk of over-leveraging their business if they don’t grow as quickly as planned, or they can lack sufficient working capital and personnel to properly manage the growth.

Meanwhile, new and emerging businesses with high-growth-potential products (e.g., breweries, kombucha, CBD products) are seeing an influx of capital during their early stages of growth, but as they grow and need larger and more risk-focused capital, they are having a hard time raising it from in-state sources.

Capital providers tend to be siloed. If investors, lenders, grantmakers, bankers, and other types of capital providers built stronger ties across the capital continuum and outside of their traditional networks, they would have a wider choice of providers to bring to the table when an entrepreneur doesn’t fit their particular criteria or needs more than one type of capital to grow. The traditional investing model is lopsided and skewed towards investor gains (or protection from losses), as opposed to being a true partnership with entrepreneurs whereby all stakeholders’ interests are considered.

and social capital are as important to food system businesses as financial capital. Having the right people and talent, networks, and connections is as critical as money to grow a business, and can assist with the transition of that business to new ownership when the time comes. Human capital is defined as the team that brings value to your organization. Social capital is the connections and shared values that exist between people and enable cooperation. When a company has developed social capital, it is much easier to access other resources such as investors, recruiting experts, or building a team. Even if a company is generating revenue and has a great team, without a network of supporters, the first bump along the way may send the company down a road they can’t recover from. The recommendations below offer ways to support entrepreneurs and their need for financial, human, and social capital.

and social capital are as important to food system businesses as financial capital. Having the right people and talent, networks, and connections is as critical as money to grow a business, and can assist with the transition of that business to new ownership when the time comes. Human capital is defined as the team that brings value to your organization. Social capital is the connections and shared values that exist between people and enable cooperation. When a company has developed social capital, it is much easier to access other resources such as investors, recruiting experts, or building a team. Even if a company is generating revenue and has a great team, without a network of supporters, the first bump along the way may send the company down a road they can’t recover from. The recommendations below offer ways to support entrepreneurs and their need for financial, human, and social capital.