Image

For generations, Vermont has been defined by dairy, an industry that has an economic impact of $2.2 billion annually and adds nearly $3 million in circulating cash daily. Wherever you are in the state, and whomever you meet, you are not far removed from the dairy sector, and the socio-economic impacts stretch well beyond the farm gate. Many farm families have been on the same piece of land for over 100 years and hold deep-seated knowledge and a connection to a specific place across time. As the current dairy crisis roils the industry, Vermont is rapidly losing the highest-value use of the working landscape, putting the agricultural land base at risk of permanent loss.

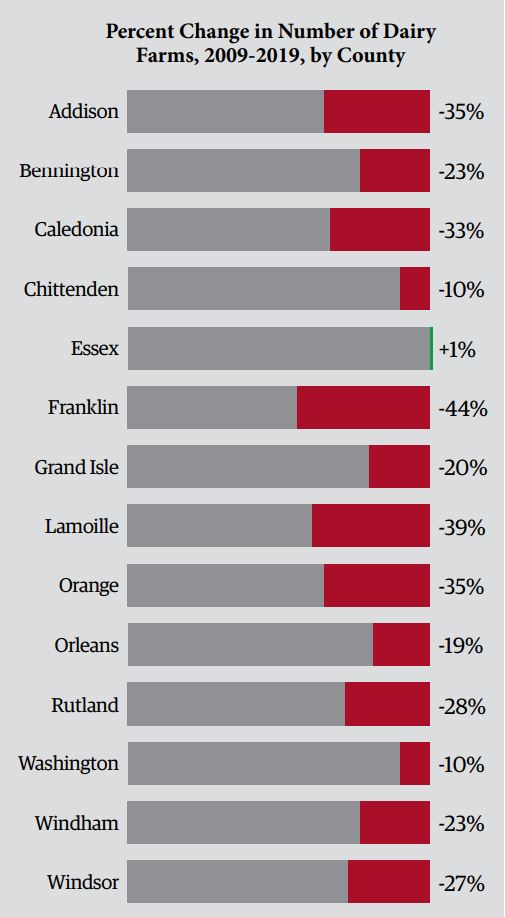

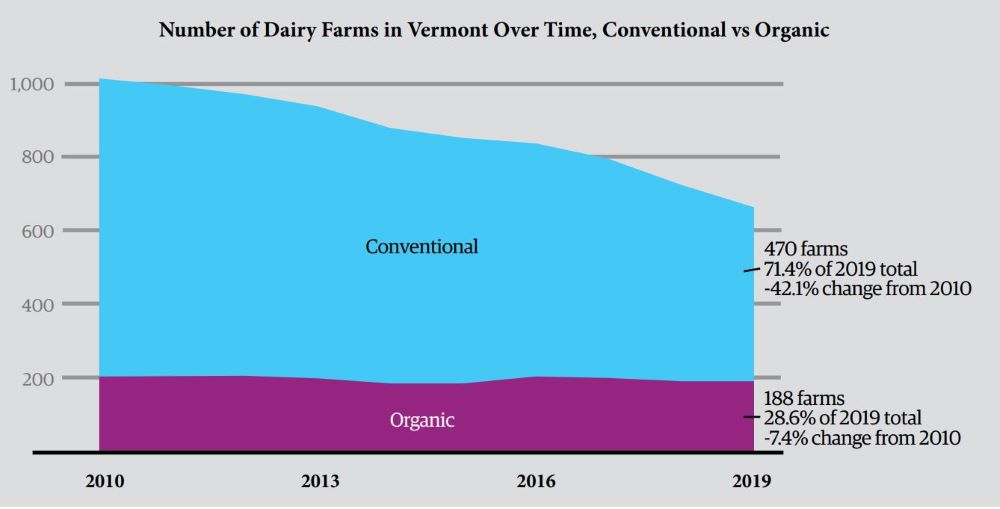

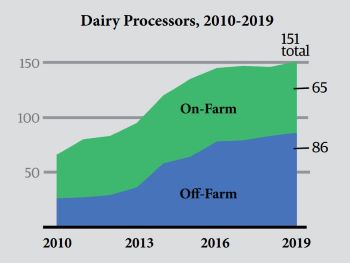

Vermont’s 664 dairy farms1 (470 conventional and 188 organic) produce about two thirds of all milk in New England, with the bulk of it being processed by one of the 151 plants into fluid milk, cheese, butter, ice cream, yogurt, and powder. In 2010, for contrast, there were 1,015 dairy farms and just 66 processors in Vermont, which is illustrative of the rapidly evolving nature of the state’s dairy sector and the success of value-added processing as a viable option.

Vermont’s 664 dairy farms1 (470 conventional and 188 organic) produce about two thirds of all milk in New England, with the bulk of it being processed by one of the 151 plants into fluid milk, cheese, butter, ice cream, yogurt, and powder. In 2010, for contrast, there were 1,015 dairy farms and just 66 processors in Vermont, which is illustrative of the rapidly evolving nature of the state’s dairy sector and the success of value-added processing as a viable option.

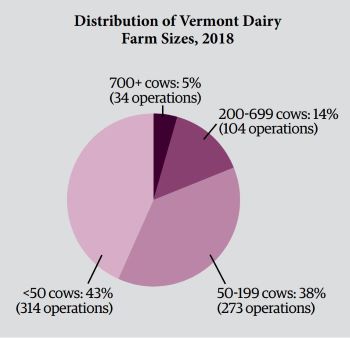

Vermont’s dairy farms encompass a variety of scales, production practices, and geographic locations. From 1,200-cow freestall facilities to 30-cow tie stall farms to 60-cow grass-based operations, Vermont’s farms run the gamut of possibilities. Unlike the rest of the nation, and making Vermont and New England unique and well-positioned to be the leader in dairy innovation, over 80% of all dairy farms milk fewer than 200 cows. The small, localized nature of the dairy sector gives it greater capacity to evolve in concert with the ever-changing dairy market.

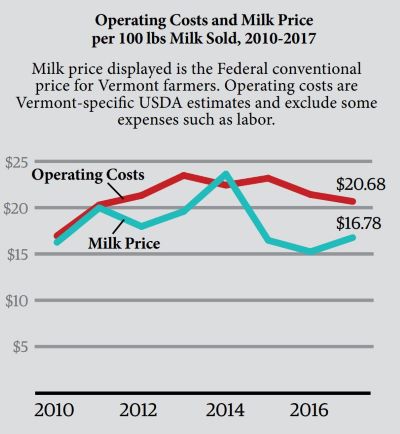

Vermont’s dairy sector, across all scales and production methods, has been impacted by the extended downturn in pricing over the past five years, which has been exacerbated by decreased exports and a changing global political landscape. While conventional milk prices have always fluctuated, typically in a three-year pattern from high to low, and organic milk had consistently higher prices over conventional, this long-term decline in both markets is having a significant impact on farms across the country as the cost of production remains at or above the price paid for milk. With the continued overabundance of milk production and record levels of processed products in storage, conventional milk price forecasts do not show a meaningful increase for potentially years to come. Organic milk is buffered to some degree from such drastic market swings, though organic producers have had production quotas and received lower prices over the past couple of years.

Dairy farmers are also faced with several other concurrent, high-stakes issues. At the forefront for Vermont are water quality and other environmental concerns, both of which are being addressed by regulations at the state and federal levels. The resulting changes to regulation have increased the financial and reporting burden for farmers. The extended downturn in pricing has led to a loss of equity for many farms and the inability to maintain equipment or infrastructure. For some farms, this has meant putting off critical water quality projects, which could exacerbate compliance issues. Finally, changing consumer preferences and a general negative public perception of dairy farming have created a perfect storm to make the current situation one of the most challenging the sector has ever experienced.

In response to the current dairy crisis, the amount of interest and work focused on the dairy industry has continued to increase and is originating from many different perspectives. Over the past two years, this work has included: Northern Tier Dairy Summit; Dairy and Water Quality Collaborative; Future of Agriculture working group; Working Lands Enterprise Initiative dairy focused funds; Vermont Milk Commission; legislative dairy farm tours; Secretary’s Dairy Advisory Committee; USDA Dairy Innovation Initiative; Payment for Ecosystem Services working group; positive dairy messaging campaign; and a dairy market assessment.

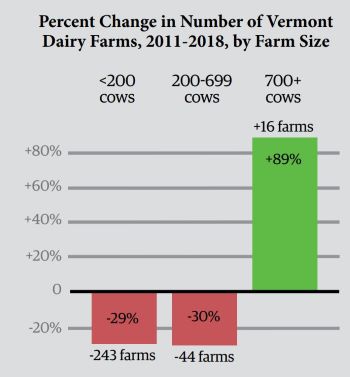

The dairy industry, much like other commodity production systems, is a least-cost production model, in which farms must get bigger and produce more for less per-unit cost in order to remain viable. As medium-sized farms increase in size, and smaller farms tend to stay small, there is a loss of farms considered “ag of the middle.” This “scale bifurcation” is leading to two opposite production systems in a commodity market which does not value differentiation of production scales. Industry information, from animal housing to nutrition to genetics, is focused on larger-scale farms and production systems, creating a gap in research and services for small farms. Essentially, large and small farms have very different needs and the national dairy industry is mostly focused on providing resources appropriate for larger farms. As Vermont’s dairy sector is primarily made up of small farms (314 farms, or 43%, had fewer than 50 cows in 2018), it is critically important that these smaller farms are positioned for success and have the opportunity to compete differently than their larger counterparts.

The dairy industry, much like other commodity production systems, is a least-cost production model, in which farms must get bigger and produce more for less per-unit cost in order to remain viable. As medium-sized farms increase in size, and smaller farms tend to stay small, there is a loss of farms considered “ag of the middle.” This “scale bifurcation” is leading to two opposite production systems in a commodity market which does not value differentiation of production scales. Industry information, from animal housing to nutrition to genetics, is focused on larger-scale farms and production systems, creating a gap in research and services for small farms. Essentially, large and small farms have very different needs and the national dairy industry is mostly focused on providing resources appropriate for larger farms. As Vermont’s dairy sector is primarily made up of small farms (314 farms, or 43%, had fewer than 50 cows in 2018), it is critically important that these smaller farms are positioned for success and have the opportunity to compete differently than their larger counterparts.

Small farms are more likely to be family run, rely on off-farm income, have multiple diversification strategies for additional income, and have fewer hired workers, which can mean that issues such as poor health and loss of income from other sources have a greater impact on these farms than on larger farms.

Small farms are more likely to be family run, rely on off-farm income, have multiple diversification strategies for additional income, and have fewer hired workers, which can mean that issues such as poor health and loss of income from other sources have a greater impact on these farms than on larger farms.The dairy marketplace is rapidly evolving as new consumer groups shape the kinds of products desired and how they are purchased. The Gen X, millennial, and Gen Z generations are pushing companies for increased transparency, relationships with producers, and values-oriented production methods, and are stepping outside of the traditional grocery store format for purchases. These generational groups are also more interested in purchasing from small to mid-scale businesses, a key area in which nearly all of Vermont dairy products squarely fit. There is a clear market opportunity for products that meet specific production criteria, including environmental standards, animal welfare conditions, and social benefits. While Vermont’s farm scale is small compared to other areas in the country, and thus is better positioned to meet consumer demands, there is a significant concern about dairy farm practices which could impact the entire supply chain as consumers move away from products that do not meet their values. Further, milk alternatives in refrigerated, shelf-stable, and frozen forms have impacted product sales and market share, a trend that does not appear to be easing in the near future.

Grass-fed dairy products, specifically those that are also organic, are the fastest growing portion of the dairy case, showing annual sales growth over 30%. Vermont is well-positioned to take advantage of this market due to the abundance of high-quality forages (plants eaten by livestock), expert technical assistance, and availability of processors who seek to enter or expand their reach into the grass-fed market. With the development of standards in labeling across industries using the grass-fed claim, consumers will be able to have confidence in their purchases. A grass and pasture-focused production strategy has additional environmental benefits, including decreased water quality concerns and improved soil health.

Since 2010, Vermont has seen a 130% increase in the number of dairy processing plants, which includes the addition of both large (e.g., Commonwealth Dairy) and small facilities (e.g., on-farm cheese makers), producing a wide variety of products that are consumed locally and exported around the world. Several of the larger facilities that are responsible for processing higher proportions of Vermont milk are owned by out-of-state companies and may also need costly upgrades to remain functional or add capacity to meet changing consumer preferences. Small processing facilities and the high-quality, award-winning products they create have pushed Vermont to the forefront of the artisanal, specialty dairy marketplace both nationally and internationally. The combination of scales of processing and the successful marketing of these products is one reason why Vermont’s dairy sector will remain relevant into the future.

Since 2010, Vermont has seen a 130% increase in the number of dairy processing plants, which includes the addition of both large (e.g., Commonwealth Dairy) and small facilities (e.g., on-farm cheese makers), producing a wide variety of products that are consumed locally and exported around the world. Several of the larger facilities that are responsible for processing higher proportions of Vermont milk are owned by out-of-state companies and may also need costly upgrades to remain functional or add capacity to meet changing consumer preferences. Small processing facilities and the high-quality, award-winning products they create have pushed Vermont to the forefront of the artisanal, specialty dairy marketplace both nationally and internationally. The combination of scales of processing and the successful marketing of these products is one reason why Vermont’s dairy sector will remain relevant into the future.

Milk pricing is a complex, federally run system that is impacted by a multitude of external forces such as commodities futures trading, product disappearance rates, and location differentials. Vermont exists in the Federal Milk Market Order (FMMO) system as part of Region 1, which also includes most of New England (excepting Maine), some of New York, Pennsylvania, New Jersey, Delaware, and some of Maryland. The FMMO system was put in place to help ensure that milk moves around the region and country in an orderly fashion, and that prices reflect distance to major milk consumption markets. Federal milk pricing sets the minimum farmers can be paid and impacts all farmers who sell into the conventional commodity stream. All processors have the ability to pay additional money for qualities they deem important (e.g., butterfat levels, milk quality) and this is the reason that organic prices are much higher, yet variable across organic processors. The Caring Dairy and Milk with Dignity programs are also examples of how processors can add money to milk checks based on farmers’ production practices meeting specific criteria.

Milk pricing is a complex, federally run system that is impacted by a multitude of external forces such as commodities futures trading, product disappearance rates, and location differentials. Vermont exists in the Federal Milk Market Order (FMMO) system as part of Region 1, which also includes most of New England (excepting Maine), some of New York, Pennsylvania, New Jersey, Delaware, and some of Maryland. The FMMO system was put in place to help ensure that milk moves around the region and country in an orderly fashion, and that prices reflect distance to major milk consumption markets. Federal milk pricing sets the minimum farmers can be paid and impacts all farmers who sell into the conventional commodity stream. All processors have the ability to pay additional money for qualities they deem important (e.g., butterfat levels, milk quality) and this is the reason that organic prices are much higher, yet variable across organic processors. The Caring Dairy and Milk with Dignity programs are also examples of how processors can add money to milk checks based on farmers’ production practices meeting specific criteria.

Vermont’s dairy farmers are actors in a system that does not account for geographic, social, environmental, or consumer considerations of farming, and thus must compete with least-cost producers in other states where mega-dairies and lax environmental regulations are the norm. Vermont has an opportunity to be the national leader for innovative and responsive solutions to the current dairy crisis and future downturns, and new policies should clearly place the state out front in addressing climate and environmental concerns while sustaining small farms. The above subtopics address some of the most pressing challenges and opportunities in the dairy sector and, while not all-inclusive of the issues facing the industry (e.g., workforce, U.S. immigration policy), lay out areas that have substantial interest and potential to change the Vermont dairy industry along a positive trajectory. The recommendations that follow build on the subtopics by providing overarching ideas for how to address the dairy sector’s most pressing needs.

Vermont’s dairy farmers are actors in a system that does not account for geographic, social, environmental, or consumer considerations of farming, and thus must compete with least-cost producers in other states where mega-dairies and lax environmental regulations are the norm. Vermont has an opportunity to be the national leader for innovative and responsive solutions to the current dairy crisis and future downturns, and new policies should clearly place the state out front in addressing climate and environmental concerns while sustaining small farms. The above subtopics address some of the most pressing challenges and opportunities in the dairy sector and, while not all-inclusive of the issues facing the industry (e.g., workforce, U.S. immigration policy), lay out areas that have substantial interest and potential to change the Vermont dairy industry along a positive trajectory. The recommendations that follow build on the subtopics by providing overarching ideas for how to address the dairy sector’s most pressing needs.